VCA#034: The Broken Mirror 📬

Clean venture capital or let it die.

👋 Welcome back, I’m Darío this is my newsletter about becoming a better venture investor and VC-backed founder.

For over a year, I’ve been researching and documenting the world’s top venture capital funds, family offices and limited partners, analyzing what makes them successful, how they operate, and the patterns that separate the best from the rest.

📝 Why the VC Model Snapped, and What’s Really Driving the New Reality

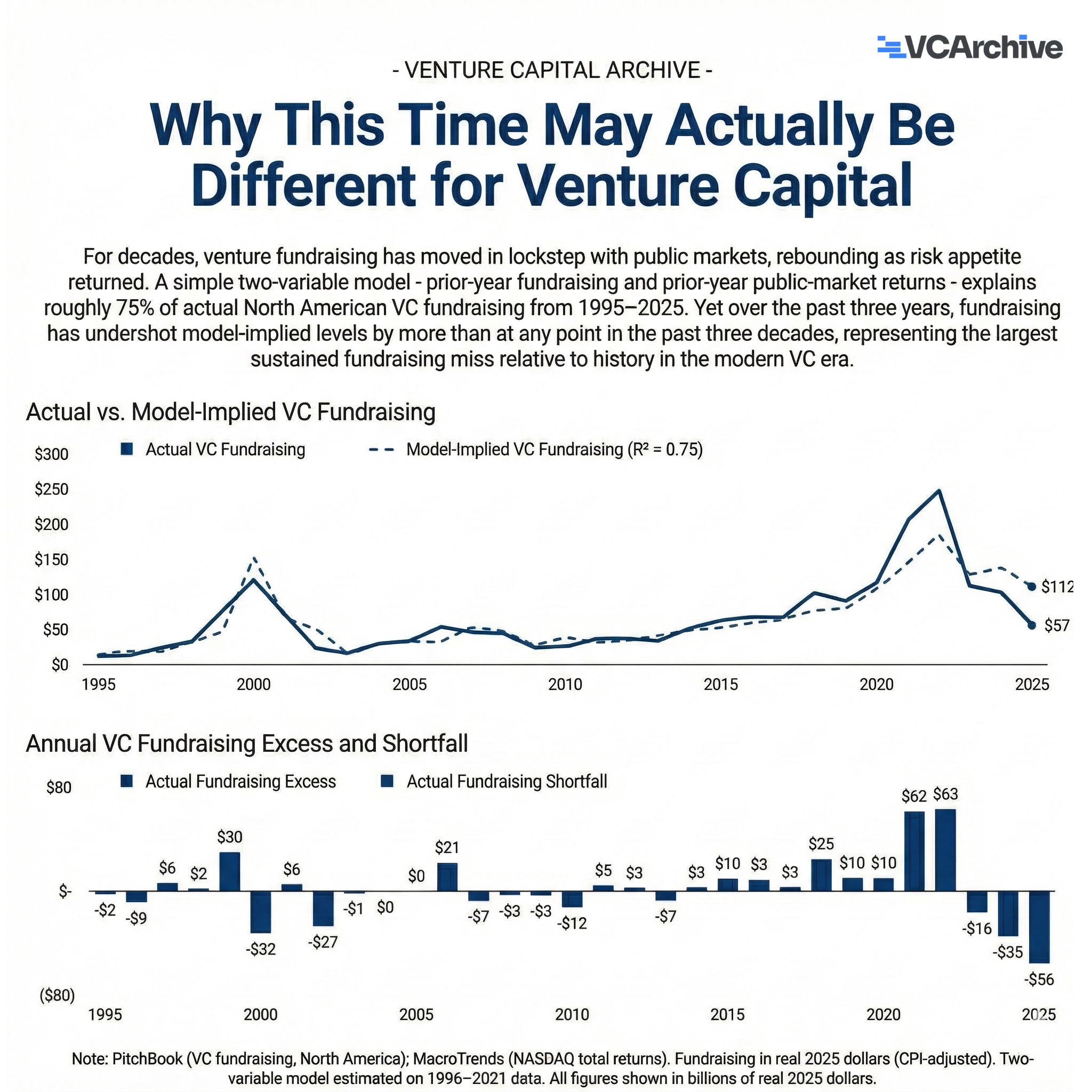

The phrase “this time is different” is usually the most dangerous four-word combination in finance. History loves to repeat itself, and cyclicality is the heartbeat of markets.

However, the data presented this year suggests that for Venture Capital, we may actually have reached a structural inflection point. For three decades, VC fundraising was a mirror of the public markets (specifically the NASDAQ). When risk appetite returned to stocks, LPs opened their checkbooks to VCs. It was a predictable, two-variable dance.

But over the last three years, that mirror shattered. As the chart shows, actual VC fundraising has dramatically undershot what the historical model implies it should be based on recent public market recovery. We are experiencing the largest sustained fundraising “miss” in the modern era.

Why has the correlation broken?

🚫 1. The Liquidity Clog (The “DPI” Crisis)

The industry’s circulatory system is backed up. LPs (investors) aren’t putting money in because they aren’t getting cash out.

The Unicorn Bubble: We have a backlog of 1,200+ Unicorns sitting on “paper valuations” from 2021 that the 2025 market refuses to pay for.

80% decrease in exits : According to 2025 our intel , liquidity fell off a cliff after the $774B peak of 2021. By 2023, distributions were down 80%, and even with the 2024–2025 AI recovery, ramains roughly 60-70% lower than the 2021 highs.

The IPO Ghost Town: In 2021, over 300 VC-backed companies went public. In 2025, that number stayed under 50 per year, representing an 85% drop in volume.

💰 2. The Deployment Paradox (The “B-Fund” Pressure)

While new fundraising is down, there is a record amount of “Dry Powder” from the ZIRP era that must be spent.

Mandated Spending: Managers of massive “B-funds” are contractually obligated to deploy billions within a fixed window, they can’t just sit on the cash.

The Distortion Effect: This “forced” capital creates valuation bubbles in “safe” or “hyped” sectors (like GenAI) while the rest of the market starves.

🌪️ 3. The New Structural Headwinds

Beyond the chart, four new forces are keeping fundraising depressed:

The Denominator Effect: Because public stocks dropped faster than private valuations were written down, many LPs are “accidentally” over-allocated to VC and cannot add more.

The End of “Free Money”: At 5% interest rates, the “hurdle rate” for a VC investment has tripled. The math for many ZIRP-era business models simply no longer works.

Secondary Market “Shadow Prices”: Shares are trading at 60% discounts on secondary markets, making it impossible for VCs to justify their “official” book values to LPs.

The Rise of Zombie Funds: ]30% of the global VCs, a generation of firms that raised big in 2021 but have zero returns are now “dead men walking,” unable to raise their next fund.

🏁 The Final Line

This isn’t a typical cycle; it’s a structural clearing event. We are waiting for the “plumbing” to unclog, meaning more down rounds, more fire sales, and a total reset of the Unicorn valuation bar.

The ecosystem needs a total cleansing. Let the 'zombies' fail. Do not deploy fresh capital until the structural mess is cleared otherwise, we are looking at a permanently broken asset class

💸 This Week’s Biggest Funding Rounds

Databricks ($4B+ Series L): The data and AI platform layer is consolidating into private-market hyperscalers before public markets can reprice them. Backers include Insight Partners, Fidelity, and J.P. Morgan Asset Management (co-leads), with Andreessen Horowitz, BlackRock, Coatue, GIC, NEA, Temasek, Thrive Capital, and T. Rowe Price. This is a bet that enterprise AI standardizes around balance-sheet scale, not architectural elegance.

Lovable (€281M / ~$330M Series B): “Vibe-coding” matures into an enterprise software factory where distribution, not developer enthusiasm, defines the moat. The round was led by CapitalG and Anthology Fund (Menlo Ventures), with NVentures (NVIDIA), Salesforce Ventures, Atlassian Ventures, HubSpot Ventures, Khosla Ventures, DST Global, plus returning Accel and Creandum.

Radiant Nuclear ($300M round): Mass-produced nuclear reactors move from theory to industrial execution. Backers include Founders Fund, Andreessen Horowitz, DCVC, General Catalyst, and Eight Roads, underwriting nuclear as scalable infrastructure rather than bespoke mega-projects.

Cyera ($400M Series E): Data security becomes the control plane for the AI enterprise. The round was led by Blackstone, with Sequoia Capital and Accel participating. Every AI deployment expands data exposure faster than productivity, making security a first-order system.

ICEYE (€233M / ~$255M Series E): High-frequency earth observation becomes core risk infrastructure for governments, insurers, and defense agencies. Led by General Catalyst, with BlackRock, Seraphim Space, and strategic investors. The category is quietly compounding into a data monopoly.

Tebra ($250M financing): AI becomes the margin engine for private medical practices. The raise includes equity led by Hildred Capital and debt from J.P. Morgan, with participation from Toba Capital, Transformation Capital, and HLM Venture Partners.

MoEngage ($180M Series F extension): Customer engagement platforms evolve into autonomous AI decision engines. The round was led by ChrysCapital and Dragon Fund, with Schroders Capital, TR Capital, and B Capital. Secondary-heavy late-stage liquidity is now the norm.

Spinny ($160M strategic financing): Scale replaces growth rate as the moat in emerging-market consumer platforms. Backers include Tiger Global, Accel, General Catalyst, and Qatar Investment Authority, funding Spinny’s acquisition of GoMechanic. Consolidation beats expansion.

QuantumDiamonds (€152M / ~$166M investment program): Quantum hardware supply chains move toward industrialization. Funded by the German Federal Ministry of Education and Research, the State of Saxony, and industrial partners including Infineon Technologies. Quantum manufacturing is treated as national infrastructure.

Imprint ($150M Series D): Co-branded credit cards are rebuilt as programmable loyalty infrastructure. The round was led by Khosla Ventures, with Thrive Capital, Ribbit Capital, Kleiner Perkins, Hedosophia, Spice Capital, and Timeless.

Chai Discovery ($130M Series B): Drug design shifts from AI hype to production tooling. The round was led by Oak HC/FT and General Catalyst, with participation from OpenAI, Thrive Capital, and Menlo Ventures.

Ambros Therapeutics ($125M Series A): Late-stage-ready biotech gets rewarded again. The round was led by RA Capital Management and Patient Square Capital (Enavate Sciences), with Abiogen Pharma, Janus Henderson Investors, Arkin Bio, Balyasny Asset Management, and Adage Capital Partners.

Mythic ($125M round): Compute-in-memory architectures re-enter the AI hardware race. Backers include SoftBank Ventures Asia, DCVC, Lux Capital, DFJ Growth, and AME Cloud Ventures, betting on power-efficient edge inference.

Atavistik Bio ($120M Series B): Genetic-driven rare-disease therapeutics attract scale capital. Backers include Foresite Capital, Venrock, RA Capital Management, and Atlas Venture.

RedotPay ($107M Series B): Stablecoin payments consolidate around distribution and licensing velocity. The round was led by Goodwater Capital, with Pantera Capital, Blockchain Capital, Circle Ventures, and HSG.

Nirvana Insurance ($100M Series D): Commercial insurance becomes a data and telematics OS. The round was led by Valor Equity Partners, with Lightspeed Venture Partners and General Catalyst increasing ownership.

Adaptive Security ($81M Series B): Human-layer security becomes AI-layer security. The round was led by Bain Capital Ventures, with NVentures (NVIDIA), OpenAI Startup Fund, Andreessen Horowitz, Capital One Ventures, and Citi Ventures.

PolyAI (€73.2M / ~$80M growth round): Enterprise voice workflows become mission-critical interfaces. Backers include Georgian, Hedosophia, Khosla Ventures, with NVentures (NVIDIA), British Business Bank, and Citi Ventures.

Fuse Energy (€59M / ~$70M round): Energy retail is recapitalized like software. The round was led by Lowercarbon Capital and Balderton Capital, with Ribbit Capital, Lakestar, Creandum, Accel, QuantumLight, and Rosberg Ventures.

Nu Quantum ($60M Series A): Quantum networking moves from theory to deployable infrastructure. The round was led by Eclipse Ventures, with Amadeus Capital Partners and IQ Capital.

Runware ($50M Series A): Real-time AI media production becomes an efficiency race. The round was led by Insight Partners, with Speedinvest.

Bound4blue ($44M round): Maritime decarbonization shifts to ROI-driven adoption. Backers include EIC Fund, CDTI Innvierte, Cassa Depositi e Prestiti, Maersk Growth, and Louis Dreyfus Armateurs.

🌱 New Venture Funds

Lightspeed Venture Partners closed $9B+ across six vehicles to back category-defining technology companies globally, spanning early-stage core funds through growth and opportunity capital. The raise formalizes Lightspeed’s multi-stage underwriting model for an AI-driven market where winners require duration, not just early conviction, backed by a diversified global institutional LP base.

Dragoneer Investment Group closed a $4.3B fund targeting late-stage, category-defining technology companies with global ambition. Designed for concentrated ownership, the vehicle reinforces the reality that private growth now absorbs much of the value creation once reserved for public markets.

Speciale Invest announced Growth Fund II (₹1,400 crore) to invest from Series A onward in Indian deeptech. The fund expands capacity to back spacetech, advanced manufacturing, energy storage, quantum, and defence-adjacent platforms as companies transition from technical validation to commercial deployment.

Viola Ventures closed ~$250M across two vehicles targeting Israeli technology leaders. Viola Ventures VII focuses on Seed and Series A investments and incubation, while Viola Conviction Fund I (~$100M) enables concentrated, secondary-led exposure to breakout portfolio companies ahead of IPO timelines.

S3 Ventures closed a $250M fund to back high-growth companies with the ability to lead rounds and reserve meaningfully through follow-ons. In a tighter market, follow-on capacity becomes a competitive weapon as exit timelines stretch.

Olympus Innovation Ventures launched Fund II ($150M) to invest in medtech startups adjacent to Olympus’ endoscopy and clinical footprint. The vehicle scales Olympus’ corporate venture allocation while maintaining a tightly product- and pipeline-linked mandate.

Kae Capital closed a $100M fund to back early-stage founders across India with sufficient reserves to maintain ownership through follow-ons. The strategy favors conviction and defense over portfolio sprawl in a more selective capital environment.

Kibo Ventures reached a €80M first close for its fourth fund (hard cap €150M) to lead Seed and Series A rounds across Europe. The fund sharpens focus on defence, space, AI, cybersecurity, and robotics, backed by BBVA Spark, CDTI Innvierte, the European Investment Fund, family offices, and portfolio founders.

FemHealth Ventures launched a $65M fund to back women’s health innovation across care delivery, diagnostics, therapeutics, and enabling infrastructure. The strategy targets a structural allocation gap in a market where unmet need and spend materially exceed venture exposure.

PSV Hafnium closed an oversubscribed €60M debut fund to back Nordic research-born deeptech companies across quantum, clean energy, and science-heavy AI. The vehicle is purpose-built for early technical conviction at the lab-to-market stage where most capital still waits for revenue proof.

Aneli Capital launched a €35M Fund I focused on robotics, medtech, ICT, space, photonics, and advanced manufacturing across the Baltics and CEE. Backed by Baltic family offices and institutional LPs, the fund aims to institutionalize deeptech formation outside Western Europe’s capital gravity.

Startuplab closed €32M Fund V to sustain Norway’s high-velocity pre-seed engine, writing $250K–$500K first cheques into 20–25 startups per year. Investors include KLP, Investinor, Nysnø, Ferd, Telenor, OBOS, and ~70 operators and founders, reinforcing an operator-aligned deployment model.

Hanoi Public Venture Capital Fund launched a $24M vehicle to catalyze Vietnam’s next wave of venture-backed companies. Positioned as a first institutional check, the fund reflects Southeast Asia’s broader shift toward public-linked capital accelerating early-stage formation.

NJEDA x CoreWeave launched the NJ AI Hub Fund ($20M) to back early-stage AI startups anchored in New Jersey’s research base, talent density, and compute access. The fund pairs capital with infrastructure, signaling that states are now competing for AI companies the way they once competed for factories.

BYT Capital launched a $19.8M fund to back emerging companies across its venture pipeline with fast decision cycles and hands-on support. At this fund size, competitive advantage is driven by speed, operator leverage, and local network access.

Rajasthan Venture Capital Fund launched India Growth Fund IV ($27.5M) to back Indian startups at the scale-up inflection point. The fund channels capital beyond Tier-1 hubs, aligning with India’s shift toward capital-efficient growth and execution-first underwriting.

Penn StartUP Fund launched a $10M university-linked fund to back commercialization and spinoffs from the University of Pennsylvania ecosystem. Built around proximity to labs, clinicians, and domain experts, the vehicle captures companies at the paper-to-prototype edge.

The Nordic Web Ventures closed $6M Fund III under Neil Murray to write first institutional cheques (~$200K) into Nordic founders across AI, robotics, and deep tech. The deliberately small AUM is optimized for speed, signal, and founder alignment.

💰 Who Got Rich This Week?

Exits, IPOs & Liquidity Moments

Medline Industries (IPO: $6.26B raise): Medline took the medical-supplies giant public after decades of private ownership, delivering one of the largest IPOs of the year. Led by Jim Boyle and backed by Blackstone, Carlyle, and Hellman & Friedman, the listing provides substantial liquidity to PE sponsors and the Mills family while positioning Medline to consolidate hospital and clinical supply chains at public-market scale.

Sobi acquires Arthrosi Therapeutics (up to $1.5B): Swedish biopharma Sobi agreed to acquire Arthrosi Therapeutics to secure a late-stage gout asset approaching Phase III. Founded by Litain Yeh, the transaction rewards Arthrosi’s VC and biotech backers and signals big pharma’s renewed willingness to pay for clinical certainty rather than early discovery risk.

NVIDIA acquires SchedMD (undisclosed): NVIDIA acquired SchedMD, the company behind Slurm, the workload scheduler that underpins a significant share of global AI and HPC clusters. Founded by Morris “Moe” Jette and Danny Auble, the deal delivers liquidity to founders and early shareholders while deepening NVIDIA’s control over the AI infrastructure software stack.

Wingify acquires Blitzllama (undisclosed, all-cash): Wingify (VWO) acquired AI-native user feedback platform Blitzllama to accelerate experimentation and product intelligence across its analytics suite. Founded by Rahul Pandey, Joel Lalgee, and Bently, the exit returns capital to seed backers including Y Combinator, Magic Fund, and 2am VC, highlighting steady M&A demand for workflow-level AI tools.

SpaceX (Secondary sale, ~$800B implied valuation): SpaceX completed a secondary share sale at roughly $421 per share, creating liquidity for employees and long-time shareholders without approaching public markets. Led by Elon Musk, the transaction reinforces how elite private companies can now offer recurring liquidity while remaining structurally private.

MoEngage (Employee tender, ~$15M): Alongside its $180M Series F extension, MoEngage facilitated a secondary tender providing liquidity to more than 250 current and former employees. Founded by Raviteja Dodda, the move reflects a broader late-stage pattern: using structured liquidity to retain talent and momentum without triggering IPO pressure.

🔥 Trending This Week

Bridgewater warns of AI investment bubble risk

Bridgewater Associates cautioned that Big Tech’s growing dependence on external capital to fuel the AI boom is “dangerous.” According to a UBS report cited by Bridgewater, AI infrastructure funding jumped from $15 billion in 2024 to $125 billion in 2025, raising concerns about whether the pace of investment is sustainable and if valuations reflect real profit prospects. ReutersAustralia’s largest pension fund shifts allocations on AI concerns

AustralianSuper, which manages A$400 billion (~US$264 billion), plans to reduce its global equities exposure for 2026, specifically citing concerns about the sustainability of the AI-driven rally. The strategy signals broader institutional caution about concentrated tech valuations and the potential for future rate hikes to weaken inflated assets. Financial TimesEurope VC funding hits third-best year on record with AI surge

Data reported this week shows that European tech VC funding in 2025 reached its third-highest level ever, with AI investment surging 161% year-on-year and all of the top eight tech hubs across Europe posting funding growth. SiftedClimate VC deals matured, not vanished

Analysis from December 2025 indicates that climate tech VC didn’t dry up instead, deal counts fell while total funding grew, reflecting more selective, higher-impact capital deployment in later-stage climate solutions. The Economic TimesIPO & M&A activity hitting record levels, shaping VC expectations

The latest Axios Pro Rata briefing reported that global M&A reached $4.39 trillion in deal value this year, up 45% from 2024, and highlighted heightened strategic activity across tech and energy. This surge in deals and continued SPAC/IPO movements is feeding into VC exit expectations for 2026. AxiosMonzo shareholder revolt highlights governance risk in VC-backed fintechs

In a high profile governance story, more than 40% of Monzo’s shareholders including major VC backers are pushing to oust the chair after the CEO’s departure. The dispute centers on board representation and strategic direction, reflecting broader concerns about governance and exit timing in VC-backed public companies. Financial TimesForbes: VC landscape in 2025 shaped by fewer seed deals and AI megadeals

Forbes’ December piece synthesizes new industry data showing fewer seed-stage rounds, increased late-stage mega-deals, and a rising role for private equity in venture allocations. These trends are foundational to how VC strategies are being re-underwritten across 2025. Forbes

📊 Recent Publications & Reports

Fresh VC-focused blogs & research:

Top 25 Travel & Tourism VC Investors – VCArchive

A Curated list of 25 travel and tourism–focused venture investors across infrastructure, consumer platforms, and climate-positive travel. Useful for founders navigating a capital-intensive, operationally complex category. Read moreQ3 2025 VC Fund Performance – Carta

Carta’s Q3 2025 performance snapshot covering IRR, TVPI, and DPI benchmarks by vintage. Read moreVenture Capital Set to Improve Globally in 2026 – Preqin

Preqin’s 2026 outlook pointing to gradual recovery in venture activity, driven by AI adoption, improving exit conditions. Read moreHow AI Is Transforming Venture Capital – Standard Metrics

A practical white paper on how AI is reshaping the VC workflow, from sourcing and diligence to portfolio monitoring and LP reporting. Read moreResponsible Investment Report 2025 – CIC

CIC’s 2025 responsible investment report outlining how ESG, stewardship, and long-term impact are integrated across its investment process. Read morePortfolio Reporting Guide – Visible

A hands-on guide to building scalable portfolio reporting, covering core metrics, and best practices for communicating performance to LPs. Read moreVenture Capital and Advanced Technologies Drive US Employment – ITIF

A policy and data-driven analysis linking venture capital investment in advanced technologies to outsized job creation and economic growth in the US. Read more

🎙️ Voices in Venture

Insights from Industry Leaders

The Twenty Minute VC – David George (General Atlantic)

A deep dive into growth investing, durability of software margins, and how late-stage investors underwrite category leaders once product-market fit is no longer the question. Listen hereInnovators and Investors – Antoni Kaniowski on Venture Building and the Future of VC

A forward-looking conversation on venture building as a repeatable system, how capital formation is shifting earlier, and why execution platforms may outperform traditional funds. Listen hereInnovators and Investors – Momentum Series: Empowering Founders to Win with Early Decisions

A practical discussion on founder leverage, early-stage decision-making, and how small structural choices compound into long-term advantage or failure. Listen hereThe Full Ratchet – Choosing the Right VC with Jiang Walsh Saxena

A tactical breakdown of how founders should assess VC value-add, board dynamics, and long-term alignment beyond brand names and headline valuations. Listen herea16z Podcast – Do Revenue and Margins Still Matter in AI?

A timely debate on whether AI companies can defy traditional unit economics or whether revenue quality and margins will ultimately reassert themselves. Listen hereEU VC – Michael Sackler on Supernode Global

An inside look at Supernode Global’s thesis, network-driven investing, and how next-generation VC platforms are being built around communities rather than capital alone. Listen here