VCA#053: Less-Is-More?

The VC playbook changed. Most founders haven't caught up yet.

👋 Welcome back, I’m Darío I study the world's top startups, VCs and family offices to document one thing: how the best actually operate.

After months of work our annual free report is live and has achieved +500 downloads!

📝 The Best VCs Are Making Fewer Bets. Here’s Why That Changes Everything.

The power law has always been venture capital’s defining feature. One or two investments generate the majority of returns. Everything else is noise. What’s changed is the intensity: in 2025, the top 1% of companies by valuation captured a third of all US venture capital. The bottom half got 7%. Deal count fell 15% while dollars invested jumped 53%.

The power law isn’t weakening. It’s becoming a power law of power laws.

The Math Problem No One Wants to Say Out Loud

A $1B fund returning 3x needs to generate $3B in exits. For a single company to return the fund, it needs a $1B exit — and that’s just to break even on the vehicle, not to generate carry. As fund sizes grow, the threshold for what “counts” rises exponentially, forcing managers into later rounds at higher valuations, competing for the same 200 deals as everyone else.

A $100M fund needs a $100M exit to return itself. That’s a company that nobody is fighting over. That’s where the real returns live.

The Data Is Not Ambiguous

Small funds ($1M–$10M) average 17.4% IRR. Large funds average 9.7%.

Only 17% of funds above $750M ever generate returns above 2.5x.

Carta’s analysis of 2,500+ funds confirms: across nearly every vintage year from 2017–2024, smaller funds posted higher IRRs than $100M+ vehicles.

In 2024, 30 firms captured 75% of all US VC fundraising. Andreessen Horowitz alone raised over 11% of the total. Their LPs are paying for brand, not performance.

a16z: The Clearest Case Study

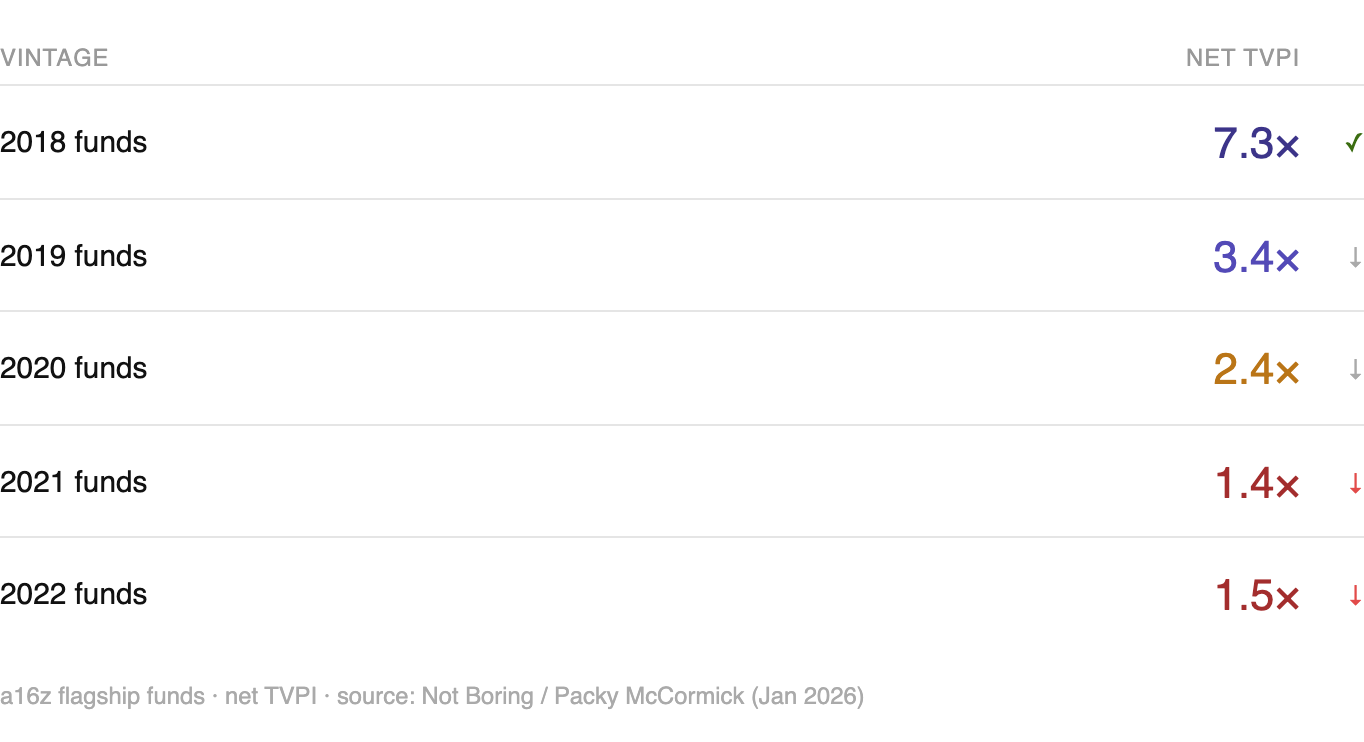

Andreessen Horowitz built one of the great VC franchises of the 2010s. Airbnb, GitHub, Lyft, Slack, Coinbase — early, contrarian, generational. The thesis was right. The returns from those vintages were exceptional.

Then they scaled. In their first era (2009–2017), they raised $6.2B across nine funds. In the second era (2018–2024), they raised $32.9B across nineteen funds in five years. The argument: if the biggest outcomes were getting bigger, you needed more capital to maintain meaningful ownership. But the TVPI tells the story:

The 2021 vintage at 1.4x TVPI — during the greatest liquidity environment in startup history — tells you everything. The crypto funds (CNK 1–4) were the outlier that proved the rule: concentrated early bets on Coinbase and the broader crypto ecosystem generated venture-like returns. Not the platform. Not the scale.

The Funds That Actually Work — and Why

Benchmark. Six partners. No analysts. Five investments per year. eBay, Uber, Twitter, Snapchat, Dropbox, Instagram. Fund sizes stay around $400–500M deliberately. When they own 10% of a company that exits at $5B, that’s $500M — the fund returned. The math works because the fund size lets every great outcome matter. Their edge isn’t selectivity for its own sake. It’s that the partnership’s network produces top-of-funnel that nobody else sees, and the fund size means they don’t need 40 bets to win.

Founders Fund. $220M fund. $18.60 returned in cash per dollar invested — one of the highest realized DPI numbers in VC history. Thiel’s bets on Facebook, Palantir, and SpaceX were made when nobody wanted them. In 2005, institutional venture capital largely ignored defense tech, hard sci-fi infrastructure, and a social network built by a 20-year-old Harvard dropout. Sequoia passed on Facebook. Most established funds had no framework for SpaceX. Palantir was considered too political, too opaque, too early. Thiel won not only because he was smarter — but because he was alone. The category had no competition. That world is gone. SpaceX’s last round had sovereign wealth funds, Tiger Global, Andreessen Horowitz, and a16z’s growth vehicles all fighting for allocation at a $350B+ valuation. The asymmetric information edge that made Founders Fund II legendary cannot be replicated when every major fund has a defense tech thesis, an AI infrastructure team, and a mandate to write $100M+ checks into the exact same companies.

First Round Capital. In 2010, First Round led a $510,000 seed check into a startup called UberCab. By the time Uber IPO’d in 2019, that investment was valued at roughly $2.5 billion — nearly 5,000 times their money. That one bet, made when Uber was a six-month-old car service in San Francisco, illustrates the firm’s entire model. First Round targets 7.5–12.5% ownership at seed, leads rounds, and deliberately vacates board seats as later investors come in — staying early, staying lean, not trying to become something bigger. Fund sizes have stayed around $150–200M across eight vehicles. The carry from Uber alone likely covered multiple funds. Uber, Square, Warby Parker, Roblox — every one of them was backed before the category was legible to larger funds. Portfolio companies have gone on to raise over $18 billion in follow-on capital collectively. First Round has never raised a mega-fund. That’s a deliberate structural choice, not a fundraising limitation.

Union Square Ventures. USV’s 2004 debut fund achieved 13.8× returns — a benchmark that allocators still study. Six of its funds from 2004 to 2016 ranked in the top quartile by Cambridge Associates benchmarks. The firm’s thesis has been consistent since founding: invest in large networks of engaged users, companies that create new behaviors and broaden access. USV’s Series A in Twitter came in 2007, when Twitter was four months old. Etsy followed in 2008, when a marketplace for handmade goods competing with Amazon seemed like a niche play. USV led the $5M Series A in Coinbase in 2013 — USV reportedly held around 7% at IPO, worth ~$6B, roughly 30× on a $200M Fund III. The firm has maintained fund sizes typically under $300M to stay nimble and focused, deploying capital across more than 130 companies. Fred Wilson has turned down the opportunity to raise larger funds explicitly and repeatedly, arguing that fund size consistency is itself a performance driver — the skills to invest a $100M fund are structurally different from those needed to manage a $1B fund.

FJ Labs. The counterintuitive case — and the most instructive one. As of late 2025, FJ Labs has invested in 917 companies, with 44 unicorns, 21 IPOs, and 139 acquisitions. In 2025 alone, it made 42 investments. Fabrice Grinda has written explicitly that the data on early-stage investing shows portfolio size correlates positively with IRR up to a point — more investments increase the probability of catching a power-law outlier. Their edge is not conviction in the traditional sense. It’s a proprietary sourcing machine built entirely around a marketplace thesis: Alibaba, Coupang, Flexport, Delivery Hero, Wallapop, Rappi — FJ Labs has amassed the world’s largest portfolio of marketplace startups, with over 30 unicorns produced from that single thesis. Volume is the strategy, but only because the thesis is tight enough to make volume coherent. It works. It doesn’t generalize to funds without an equally specific and defensible domain edge.

Why the Power Law Got More Extreme

Three structural shifts have made the generalist mega-fund model increasingly unworkable:

Winners stay private longer. OpenAI, Anthropic, Stripe, SpaceX, Databricks — all generating $1B+ in revenue, all still private. Returns that used to arrive in year 7–10 now arrive in year 12–15, or don’t arrive at all. Paper gains sit on balance sheets while LPs wait for DPI that keeps not coming.

The biggest rounds happen earlier. Median Series A valuations for AI startups exceeded $50M in 2025. To generate a 10x from a $50M entry, you need a $500M exit — in a market where only 1.5% of VC-backed companies ever reach $100M in revenue. The math doesn’t work unless you’re getting into the absolute winners, and the absolute winners are now being priced like they’ve already won.

Winner-take-most is more absolute than ever. In the 1990s, Google, Yahoo, and Ask coexisted. Today the top AI infrastructure company will capture 80%+ of category value. Being second in foundation models is not a business. Being second in cloud is AWS’s charity work. For a generalist fund writing into 60 companies across every sector, the probability that any given check lands in the actual category winner — not just a good company — is vanishingly small.

The Structural Trap

The 30 firms that captured 75% of LP capital in 2025 are running a different business than venture capital. They live on management fees — 2% on $1B is $20M a year to run the firm, regardless of returns. They optimize for AUM, not carry. Their incentive is to raise the next fund, which requires showing enough paper gains to stay in LP conversations, not necessarily to generate DPI.

Small funds can’t live on fees. 2% of a $100M fund is $2M — barely enough for a lean team. They live or die on carry. Their incentive is perfectly aligned with LP returns.

This is not a new insight. But the data confirms it with increasing clarity every vintage year: the firms with the most capital are generating the worst returns, and the firms with the least capital are generating the best.

The power law hasn’t changed. What’s changed is how extreme it’s become, how early the concentration happens, and how much capital is now chasing the same handful of outcomes. In that environment, fund size isn’t a competitive advantage. It’s a constraint that makes the math of venture capital structurally harder to solve — and the generalist mega-fund model is bearing the cost.

🔥 Trending This Week

1. The Non-AI Startup Has a New Fundraising Reality. Here’s What Actually Works.

The market has made its preferences clear. Founders must now prove distribution advantage, not just traction. Investors are digging deeper into repeatable sales engines, proprietary workflows, and deep subject matter expertise that holds up against the capital arms race.

For founders building outside AI — in climate, biotech, fintech, consumer, enterprise SaaS — a new set of rules is hardening:

Revenue is the new pitch deck. Traction requirements that used to apply at Series B now apply at seed. The seed funding environment in 2026 mirrors what Series A looked like a few years ago — investors are more selective, competition is fiercer, and the bar for traction has risen significantly.

The AI wrapper is not optional. 81% of early-stage European cloud companies are now AI-native, up from 50% a year ago. Founders who can credibly embed AI into their core product — even modestly — are seeing materially faster processes and better terms.

The Series A gap has become a Series A wall. For the 2022 seed cohort, only 20% of companies have graduated beyond seed — compared to 51%–61% for companies from earlier years. The funnel has compressed by more than half in four years.

Bridge rounds are back. With IPO windows uncertain and the Series B bar elevated, founders are building 18-month extensions rather than chasing the next institutional round on someone else’s timeline. The data shows this is not a failure signal — it’s increasingly the norm.

Geography remains the most underused lever. Non-AI founders in MENA, Southeast Asia, CEE, and the Nordics are finding meaningfully less competition for LP attention and more receptive regional funds than their US counterparts. The market isn’t global. The opportunity is.

2. AI Took 73 Cents of Every US Venture Dollar in April. The Rest of the Market Is Running Out of Road.

US startups raised $20.8B across 442 deals in April 2026, up 63.9% in capital and 21.1% in deal count year-over-year. AI companies attracted 73% of all capital — $15.18B across 189 deals. Project Prometheus’s $10B raise alone accounted for 48% of national capital deployed.

Strip out the mega-rounds and a structural problem comes into focus: adjusted for inflation, non-AI venture funding in Q1 2026 was actually below Q1 2020 levels. The impact is already visible in hiring data, runway extensions, and pivot announcements. Multiple SaaS companies that raised Series B rounds in 2023 and 2024 are now struggling to close follow-on funding as investors redirect attention and capital toward AI infrastructure.

The math for non-AI seed founders is getting worse fast. Only 15.4% of startups that raised a seed round in early 2022 were able to raise a Series A within two years, compared to 30.6% of companies that managed this in 2018 — a 50% drop in success rates. Seed-stage AI startups now receive valuations approximately 42% higher than non-AI peers, compressing the denominator for everyone else.

The bifurcation is structural, not cyclical. If you don’t have an AI angle, you’re competing for a shrinking pool of attention from a finite number of partners. The market isn’t closed. It’s just closed for most people.

3. The Windsurf Saga Is Over — and It Tells You Everything About the AI Coding War.

The original story was simple: OpenAI would acquire Windsurf for $3B at 75x ARR on $40M revenue — strategic necessity masquerading as financial logic, after Cursor’s parent company refused to sell even at a $9B valuation.

What actually happened is more instructive. OpenAI’s $3B acquisition collapsed after Microsoft demanded IP rights to Windsurf’s technology — which would have directly competed with GitHub Copilot. After the exclusivity period expired, Google moved in with a $2.4B licensing and acquihire deal, taking CEO Varun Mohan, co-founder Douglas Chen, and approximately 40 core engineers. Three days later, Cognition — the maker of Devin — acquired the remaining IP, product, brand, and ~210 employees for an estimated $250M. At the time of the split, Windsurf had reached approximately $82M in ARR.

The deal’s collapse revealed the real constraint: Microsoft’s control over OpenAI’s developer distribution is a structural ceiling that forces OpenAI into acquisitions Microsoft can veto. The war for the AI coding layer is now a three-way fight between Microsoft (GitHub Copilot + IDE distribution), Google (DeepMind talent + Antigravity), and the independent ecosystem (Cursor at $9B valuation, ~$300M ARR; Cognition absorbing Windsurf). Cognition’s ARR has more than doubled since the acquisition, with a $25 billion valuation as of April 2026.

The IDE is the new browser. The question is who owns the on-ramp to the agentic economy — and right now, nobody has won.

4. Europe’s VC Numbers Look Better. The Structural Problem Is Getting Worse.

The headline is positive: European venture funding reached $17.6 billion in Q1 2026, up nearly 30% year over year and marking the second consecutive quarter of growth. AI, for the first time, claimed more than 50% of Europe’s total funding for the quarter. Three new frontier labs — Recursive Superintelligence and Ineffable Intelligence in London, and Yann LeCun’s Advanced Machine Intelligence in Paris — collectively raised $2.6B.

But behind the headline, the same structural bifurcation is deepening. Deal volume plummeted 40% year over year. Seed-stage deals fell 44% and early-stage deals fell 30%, while late-stage volume held flat. More money, far fewer companies receiving it.

The deeper problem is LP infrastructure. European pension funds allocate just 0.02% of their assets to venture capital, compared with 1.9% in the United States. Finch Capital estimates that without American late-stage capital, Europe would face a €9 billion shortfall in the funding required to scale its breakout companies.

The EIF is trying to close the gap: it is launching a €15B fund of funds to back growth-stage VC across Europe, targeting up to €200M tickets per company. Whether that gets deployed fast enough to matter for the current generation of European AI labs is a different question. Europe has world-class research talent. It doesn’t yet have the capital infrastructure to keep it. That gap is the defining structural challenge of 2026 — and nobody has a convincing answer yet.

5. The US-China Tariff Truce Has a Deadline. And Both Sides Disagree on What They Agreed.

On May 12, the US and China reduced tariffs to 30% and 10% respectively. The S&P 500 jumped 3%, the Nasdaq nearly 4% — its fastest single-day recovery since Liberation Day in April. Trump landed in Beijing on May 13 for his first face-to-face meeting with Xi since 2017.

Then came the asterisks. The US and China came away from the summit touting different versions of what had been agreed: the US cited trade deals; China said it had warned Washington over Taiwan. Neither side confirmed the other’s claims.

For venture, the immediate read is cautiously positive — hardware and supply chain startups see input costs ease, cross-border pipelines frozen since April can start to thaw, and Chinese AI startups gain some breathing room on rare earth controls.

💸 This Week’s Startup Funding Rounds

🏔️ Growth & Mega Rounds

Anduril Industries ($5B, Series H at $61B valuation): Newport Beach-based defense-tech company building autonomous military systems across air, sea, and land. Led by Thrive Capital and Andreessen Horowitz, Anduril is increasingly operating like a next-generation defense prime rather than a traditional startup.

Infinite Reality ($3B, Strategic): Immersive AI and digital-media infrastructure company scaling virtual experience ecosystems and AI-native media platforms. The round reflects growing investor concentration around distribution-layer AI businesses.

Isomorphic Labs ($2.1B, Series B): London-based AI drug discovery company founded by Demis Hassabis. Backed by Thrive Capital and Alphabet, the company is positioning AI as core scientific infrastructure rather than software tooling.

Firmus Technologies ($2B, Pre-IPO Financing): Australian AI data-center infrastructure company backed by Regal Capital and UniSuper. AI infrastructure is increasingly being financed like sovereign industrial capacity.

Sierra ($950M, Series E at $15B valuation): San Francisco-based enterprise AI agent platform founded by Bret Taylor and Clay Bavor. Backed by Tiger Global, GV, Benchmark, Sequoia, and Greenoaks.

🌵 Series D & Late Stage

Quantum Systems ($680M, Late Stage): German aerospace and drone company reportedly backed by Airbus and Blackstone. Europe is accelerating investment into sovereign defense infrastructure.

Recursive Superintelligence ($650M, Growth at $4.65B valuation): Frontier AI lab founded by former DeepMind and OpenAI researchers. One of Europe’s most ambitious attempts to build an independent frontier model company.

Mind Robotics ($400M, Growth): Palo Alto-based robotics startup spun out from Rivian. The company builds AI-enabled industrial robotics systems for manufacturing and logistics.

Cowboy Space Corporation ($275M, Series B at $2B valuation): Space infrastructure company founded by Robinhood co-founder Baiju Bhatt. Focused on orbital compute infrastructure and space-based data centers.

Anagram Therapeutics ($250M, Growth): Massachusetts-based biotech developing therapies for exocrine pancreatic insufficiency. Backed by Blackstone Life Sciences.

Fractile ($220M, Series B): London-based AI inference-chip startup backed by Accel and Founders Fund. Building SRAM-based chips optimized for frontier-model inference efficiency.

Windward Bio ($165M, Growth): Immunology and inflammatory-disease biotech backed by OrbiMed and Novo Holdings. Precision therapeutics remains one of biotech’s strongest funding categories.

Oishii ($150M, Series C): Jersey City-based vertical farming company integrating robotics and automation into indoor agriculture. One of the few vertical-farming companies successfully scaling post-downturn.

Panthalassa ($140M, Series B at $1B valuation): Climate-tech startup combining offshore wave energy with AI compute infrastructure. AI’s energy bottleneck is creating entirely new infrastructure categories.

Exaforce ($125M, Series B at $725M valuation): AI-native cybersecurity company backed by HarbourVest, Peak XV, and Khosla Ventures. The platform uses autonomous AI agents to manage real-time security operations.

Create Medicines ($122M, Series B): Biotech company developing in vivo immunotherapies for autoimmune disease and cancer. Backed by ARCH Venture Partners and Hatteras Venture Partners.

🌴 Series C

VoltaGrid ($1B, Strategic Financing): Houston-based energy infrastructure company backed by Halliburton and Blackstone. Provides mobile natural-gas power systems for AI data centers.

waterdrop® ($113M+, Growth): Vienna-based hydration company backed by Aspeya and Atlantic Grupa. One of Europe’s largest profitable consumer-brand raises this year.

HavocAI ($100M, Series A): Rhode Island-based autonomous systems company building military and commercial autonomy platforms. Defense autonomy is rapidly becoming a core venture category.

Turion Space ($75M+, Series B): Space infrastructure company building orbital servicing and logistics systems. Focused on the growing satellite-maintenance economy.

🌲 Series B

Star Catcher Industries ($65M, Series A): Florida-based startup building orbital solar-energy transmission systems for satellites. Focused on solving power constraints for orbital infrastructure.

Tessera Labs ($60M, Series B): San Jose-based multi-agent AI platform automating ERP modernization across SAP and Oracle systems. Led by Andreessen Horowitz.

UroMems ($60M, Growth): French implantable-medical-device startup targeting urinary incontinence. One of Europe’s largest medtech financings this week.

Astrocade ($56M, Series C): Los Altos-based generative AI gaming platform backed by Sequoia Capital and Sea Group. A notable example of Southeast Asian capital co-leading US AI rounds.

Vapi ($50M, Series B): San Francisco-based API-native voice AI infrastructure platform. Voice agents are emerging as one of AI’s strongest workflow categories.

Mantle8 ($35M, Growth): French natural-hydrogen exploration startup betting on geological hydrogen as scalable zero-emission energy.

Embat ($34M, Series B): Madrid-based AI-native treasury-management platform integrating with more than 15,000 banks and ERP systems. European fintech is shifting toward institutional infrastructure.

🌳 Series A

Bluefish AI ($20M, Series A): AI-native search optimization platform backed by NEA and Salesforce Ventures. Focused on helping brands compete inside AI-native discovery systems.

Spektr ($20M, Series A): Copenhagen-based compliance automation startup backed by NEA and Northzone. Building AI-native infrastructure for financial institutions.

Tracebit ($20M, Series A): Cloud-security startup backed by FirstMark and Accel. Focused on deception-based infrastructure for AI-native cyberattack environments.

🌿 Seed

Entire ($60M, Seed at $300M valuation): AI-native developer platform founded by former GitHub CEO Thomas Dohmke. One of the largest AI seed rounds of the year, reflecting investor appetite for autonomous software-engineering infrastructure.

Ciroos ($21M, Seed): AI SRE infrastructure platform building autonomous agents for incident response and operations teams. Founded by former Cisco and AppDynamics executives.

Ciridae ($20M, Seed): AI transformation platform founded by former Andreessen Horowitz and Apple operators. Focused on bringing AI infrastructure to industrial and mid-market businesses.

Standard Kernel ($20M, Seed): AI infrastructure startup building software that automatically optimizes GPU kernels for frontier AI workloads. Focused on reducing inference costs without changing hardware.

🌱 New Venture Funds

Week of May 9–15, 2026

S2G Investments has raised $1B for its first fund since spinning out independently from Builders Vision. The vehicle targets climate resilience, agriculture, energy systems, and industrial infrastructure - sectors increasingly benefiting from geopolitical fragmentation and industrial policy tailwinds.

Lightrock has launched a $500M climate and energy-transition fund targeting electrification, clean mobility, and sustainable industrial systems. The strategy reflects how climate venture capital is consolidating around infrastructure-scale economics rather than ESG narratives alone.

A* has closed Fund III at $450M, focused on early-stage AI, fintech, healthcare, and infrastructure software startups. Led by Kevin Hartz and team, the firm continues to position itself as a concentrated conviction-driven alternative to the era of oversized AI megafunds.

Mettle Capital is targeting a $350M–$400M debut fund focused on Indian AI, software, and consumer internet startups. Founded by former Peak XV leaders Ashish Agrawal, Ishaan Mittal, and Tejeshwi Sharma, the launch reflects the ongoing decentralization of India’s venture ecosystem post-Sequoia split.

Duration Ventures is raising a $375M debut fund focused on enterprise AI infrastructure and application-layer software. Founded by former leaders from Lightspeed and General Catalyst, the firm highlights how experienced operators still command LP demand despite a difficult fundraising market.

Silicon Road Ventures has launched a $17.6M AI-focused fund targeting commerce infrastructure and agentic AI startups in India. The thesis is notable for focusing less on horizontal copilots and more on workflow-native automation embedded inside enterprise systems.

Lansdowne Partners has launched a $147M first close for a new venture vehicle backing UK university spinouts and deeptech companies. The strategy reflects growing investor appetite for sovereign research commercialization and defensible scientific IP emerging from Europe’s academic ecosystem.

Kalos Ventures has debuted with a $78.8M inaugural fund focused on applied AI, enterprise software, and frontier technologies. The firm is positioning itself around pragmatic AI adoption rather than foundation-model speculation, reflecting a broader shift toward commercially deployable infrastructure.

Khwarizmi Ventures has launched Fund II with a first close exceeding $70M to back startups across Saudi Arabia and the GCC. The firm continues to focus on fintech, AI, and digital infrastructure as Gulf ecosystems mature into independent capital markets with growing regional LP participation.

Restive Ventures has closed Fund III at $45M, continuing its focus on fintech, healthcare, and enterprise software startups outside Silicon Valley. The firm remains one of the more consistent proponents of distributed venture investing, backing founders in overlooked US markets long before it became fashionable.

Skinos Ventures has launched Fund I at $26M to back early-stage startups across Southern Europe, with a focus on founders operating outside traditional European capital hubs. The emergence of smaller geography-specific funds continues to reinforce the fragmentation of Europe’s venture landscape into regional micro-networks.

📈 IPO Debuts (Priced & Traded This Week)

Cerebras Systems (NASDAQ: CBRS, $5.55B at $185/share, May 14): The Nvidia challenger priced at $185, well above its $150–$160 range on the back of 20x oversubscription, opened at $350, and closed day one up 68% at $311.07, giving it a $95B market cap. The largest US tech IPO since Uber’s 2019 debut. Founded in 2016 by Andrew Feldman and Sean Lie around a wafer-scale AI chip that promises inference 15x faster than GPUs.

Who got rich:

Andrew Feldman (CEO, stake worth $3.2B at close)

Sean Lie (CTO, stake worth $1.7B at close)

Fidelity (largest institutional holder, stake worth $5.5B at open)

Benchmark via Eric Vishria (co-led Series A in 2016, stake worth ~$6B at open)

Foundation Capital via Steve Vassallo ($37M invested, stake worth ~$5.3B at open 76x return)

Eclipse via Lior Susan (stake worth ~$5.2B at open)

Alpha Wave Global (6.5% stake)

Sam Altman and Greg Brockman (personal angel stakes worth $27.8M and $24.2M at close)

Intel CEO Lip-Bu Tan (angel investor)

Morgan Stanley, Citigroup, Barclays, UBS (underwriters)

Blackstone Digital Infrastructure Trust (NYSE: BXDC, $1.75B at $20/share, May 14): Blackstone launched a newly-formed REIT targeting AI-era data center assets leased to hyperscalers on long-term contracts. Raised $1.75B from 87.5M shares; overallotment option could push total to $2B. A Blackstone affiliate self-anchored $200M of the deal. IPO investors receive a 1% bonus share grant, implying an effective price of $19.80.

Who got rich: Blackstone (sponsor, earns management fees and the economic upside of the platform), Goldman Sachs, Citi, Morgan Stanley, Barclays, BofA, JPMorgan (underwriters).

EagleRock Land (NYSE: EROK, $320M at $18.50/share, May 14): Permian Basin land royalty company controlling 236,000 acres in the core Delaware and Midland sub-basins priced 17.3M shares at $18.50, at the midpoint of its $17–$20 range. Collects royalties and surface fees from oil, gas, and increasingly from AI data center and power infrastructure buildout on its acreage.

Who got rich: Existing owners (retained ~80.8% of voting power post-IPO), Goldman Sachs, Barclays, JPMorgan (bookrunners).

🤝🏻 M&A & Strategic Liquidity

Roche acquires PathAI (up to $1.05B, announced May 7): The Swiss diagnostics giant pays $750M upfront plus up to $300M in milestones for the Boston-based AI digital pathology startup. A five-year partnership converted into a full strategic exit. Close expected H2 2026.

Who got rich: Andy Beck (CEO and co-founder), Aditya Khosla (co-founder), General Catalyst (led Series A), General Atlantic (led Series B), D1 Capital Partners and Kaiser Permanente (co-led $165M Series C), Tiger Global, 8VC, Labcorp, Bristol-Myers Squibb, and Merck GHI.

Bullish acquires Equiniti from Siris Capital ($4.2B, announced May 5): Crypto exchange Bullish (NYSE: BLSH), run by Tom Farley, agreed to buy one of the world’s largest share registry and transfer agent businesses serving 35% of the S&P 500 and 50% of the FTSE 100, to build the infrastructure layer for tokenized securities.

Who got rich: Siris Capital (PE seller, full exit), Tom Farley and Bullish management (strategic architects of the deal), Equiniti leadership on close.

OnlyFans sells 16% stake to Architect Capital at $3.15B valuation (May 8): Fenix International, the UK operator of OnlyFans, sold a minority stake for $535M weeks after founder Leonid Radvinsky died of cancer at 43. His widow Yekaterina Chudnovsky assumed control and moved quickly to bring in outside capital. James Packer and Sam Lessin co-invested alongside Architect Capital.

Who got rich: The Radvinsky estate and Chudnovsky family (partial liquidity at a clean valuation marker), Architect Capital (gains exposure to one of the most cash-generative creator platforms on earth), James Packer and Sam Lessin (co-investors in the deal).

📈 IPOs on Deck (Imminent Listings)

Spring Valley Acquisition Corp. III (SVAC): In active de-SPAC discussions with General Fusion, with the company publicly outlining LM26 commercial fusion milestones this week - the most concrete public signal yet that a fusion company intends to go public via SPAC in 2026.

OpenAI is preparing for a Q4 2026 IPO targeting a near-$1T valuation, per WSJ, aiming to beat Anthropic to market. Sam Altman’s trial against Elon Musk concluded closing arguments this week; jury deliberations begin Monday.

SpaceX IPO remains the most anticipated offering of the decade, widely expected H2 2026 or 2027. 137 Ventures has now accumulated a SpaceX stake exceeding $10B across two dozen rounds since 2010.

📊 Recent Publications & Reports

Fresh VC-focused blogs & research:

25 Active Family Offices in Portugal – VC Archive A curated map of Portugal’s most active family office investors, direct-use intelligence for GPs raising in the Iberian market. Read more

30 Best Active Space & SpaceTech VCs in 2026 – VC Archive The 30 most active investors writing checks into the orbital economy, published the same week the sector raised over $1B in new rounds. Read more

Why Senior VC Partners Are Leaving Big Firms for Smaller Funds – VC Archive The structural forces behind the spinout wave, ownership economics, mandate freedom, and the limits of platform scale. Read more

Why VCs Keep Changing Their Mind About What’s Hot and Not – VC Archive How venture conviction cycles work from contrarian to consensus to embarrassing and what founders should actually do with that information. Read more

Branding for Venture Capital vs. Startups – VC Archive Two different games, two different audiences, why most funds get it wrong by borrowing the startup playbook. Read more

The Future of Venture Capital: Unlocking Liquidity and Growth – World Economic Forum A structural assessment of the $3.5T VC industry, slowing capital recycling, uneven global scale-up distribution, and five priorities to keep the model viable. Read more

More Than the Eye Can VC: What’s Trending in 2026 – Tech Brew / Fidelity Private Shares How VCs are actually moving in 2026, shorter diligence, harder terms, and a widening gap between AI-native companies and everything else. Read more

Innovation Ecosystems and Entrepreneurial Venture Capital: Evidence from European Countries – Open Research Europe / EC Peer-reviewed analysis of 28 EU countries showing bidirectional causality between VC activity and patents, R&D, human capital, and government effectiveness, early-stage VC is the most sensitive variable. Read more

🎙️ Voices in Venture

Insights from Industry Leaders

20VC – Cliff Weitzman / Speechify What Weitzman learned studying 100 top CEOs, living with MrBeast, and building Speechify through obsessive, unconventional leadership. Listen here

The Innovators & Investors Podcast – Applying Global Brand Platforms to Early-Stage Growth How founders should build brand architecture before they have the scale to enforce it, so it doesn’t need to be rebuilt at Series B. Listen here

The Full Ratchet – Investor Stories 475: What Makes Founders Exceptional Ben Ortlieb, David Ulevitch, and Jake Saper on the most visionary founders they’ve backed and what intensity and conviction actually look like up close. Listen here

Kstreet VC Podcast – How VCs Evaluate Founding Teams Paige Soya and Nick Duafala break down the real framework behind team diligence, what signals move deals forward and what kills them. Listen here

a16z Podcast – AI Agents, Enterprise Workflows and The Future of SaaS Aaron Levie, Martin Casado, and Steve Sinofsky on what happens to enterprise software when agents become the primary users and why incumbents may be more resilient than the narrative suggests. Listen here

Acquired – Ferrari How 79 years of radical scarcity built the world’s most powerful luxury brand and why intentional restraint is the counterintuitive lesson every premium founder needs to hear. Listen here

Invest Like the Best – The Private Markets Reckoning David George (a16z) on why $5 trillion in tech market cap now sits in private markets, up 10x in a decade, and what it means for founders, LPs, and venture liquidity. Listen here