VCA#061: The Headwind

When the market turns against you, the only edge left is how prepared you are

👋 Welcome back, I’m Darío I study the world's top startups, VCs and family offices to document one thing: how the best actually operate.

After months of work our free Annual Report 2025 is live and has achieved +1000 downloads!

🔥 What Moved the Needle This Week

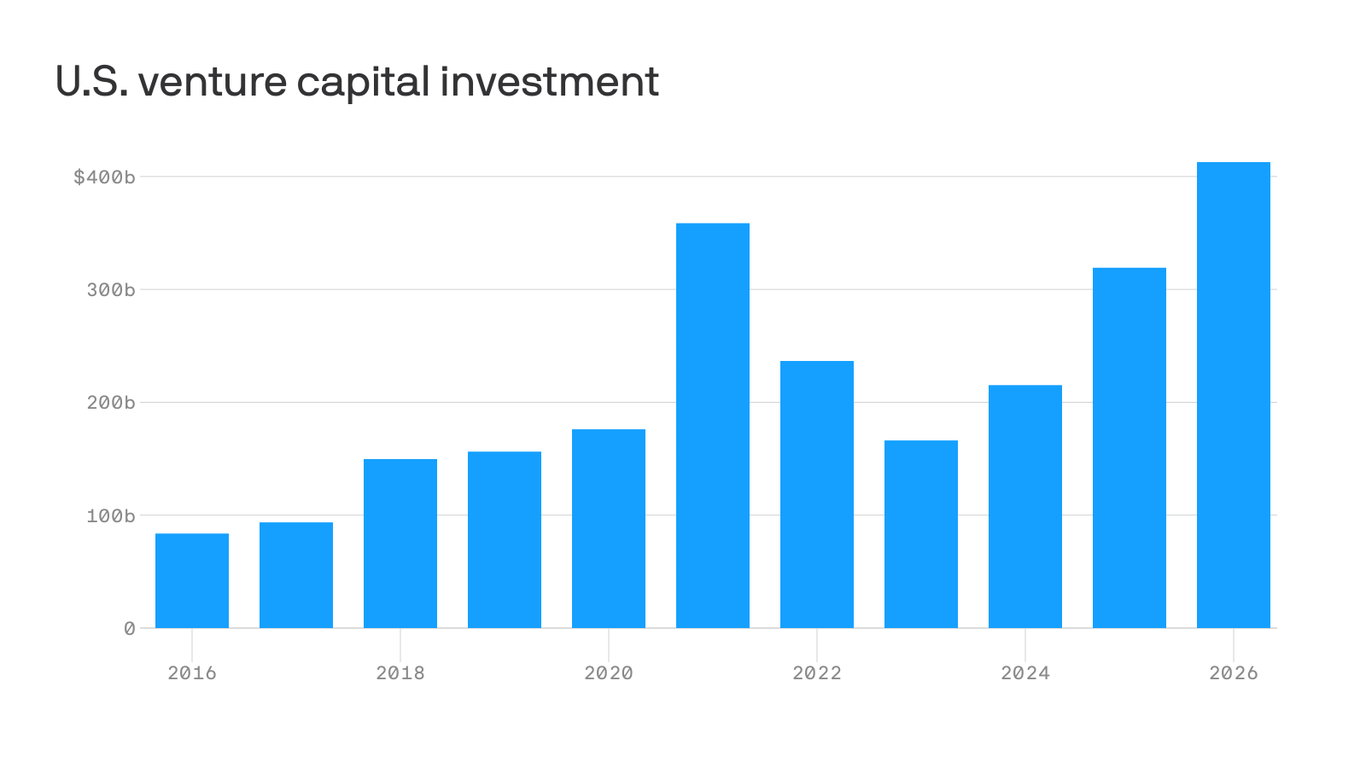

1. $510B in six months. Venture capital just had its best half-year in history.

Global startups raised $510B in H1 2026 which is more than the entire $440B raised across all of 2025. US companies alone pulled in $412.7B, up 29% year over year.

The numbers sound extraordinary until you look at where the money actually went. AI captured roughly 80 to 86% of all venture dollars and just two companies, OpenAI and Anthropic, absorbed $217B between them which is 43% of all global startup funding. Every other startup on the planet globally shared what two companies left behind.

2. The UK just quietly had its best fundraising year on record and most people missed it.

Against a backdrop of American AI concentration, the UK quietly had its best fundraising period on record. $17B raised in H1 2026, double the year before. Defence tech, fintech, and AI infrastructure are driving it. For European fund managers who spent the last two years hearing that LP capital was all flowing to the US, this is the data point worth carrying into your next LP meeting.

3. California took 10x more VC than any other US state. The concentration story inside the concentration story.

California pulled in $335B while New York, the second biggest market, raised $11.5B. It raises a real question about whether venture capital is quietly becoming a California only asset class with satellite offices everywhere else just along for the ride.

4. Corporate VCs are disappearing from deals. Here’s what’s actually happening.

CVCs participated in just 21.1% of US deals this year, the lowest in a decade. The story isn’t that corporations are pulling back. It’s that they’re bypassing their venture arms entirely for direct AI infrastructure investments handled at the C-suite level. For founders who relied on strategic corporate investors as a signal in their rounds, that signal is getting harder to come by.

📝The Founder Who Raised in a Bad Market

Elena had eighteen months of runway when she decided to start raising. By the time she opened her first investor conversation she had eleven. By the time she got her first term sheet she had six. And by the time the round closed she had four.

She’ll tell you it was the hardest thing she’s ever done. She’ll also tell you she’d do it exactly the same way again.

This is not a feel good story about grit and persistence. It’s a forensic look at the specific decisions she made that separated her from the founders who ran the same process in the same market and came back empty handed.

She stopped pitching and started qualifying

The first thing Elena did differently was something most founders resist. She narrowed the list. While the founders around her were sending decks to every fund they could find and booking forty intro calls a month she was talking to twelve investors and only twelve. Every single one of them had written a check at her stage in her sector in the last eighteen months. Every single one had dry powder. She knew this before she picked up the phone.

59% of founders say market conditions had a medium to large impact on how they approached funding in 2025. Most responded by widening the funnel. Elena responded by tightening it and the math worked out in her favor because a warm conversation with the right fund closes faster than twenty lukewarm conversations with the wrong ones.

She reframed the story around the market not the product

The second thing she did was harder. She rewrote the pitch.

Not the deck itself but the central argument. In a normal market she would have led with product vision and market size and growth trajectory. In this market she led with why her company was built for exactly this moment and why the conditions that made other companies fragile made hers stronger.

Investors in a down market are more interested in companies with long term defensibility than those promising immediate returns and Elena understood this earlier than most. She didn’t hide from the macro environment. She made it her strongest slide.

She ran the raise like a sales process

The third thing was operational. Elena treated the fundraise the way she treated a sales pipeline because that’s exactly what it is. She had a tracker. She had defined stages. She had a clear sense of where every conversation was in the process and what the next action was for each one. She sent follow ups within 24 hours of every meeting. She shared updates proactively every three weeks whether or not she’d been asked.

Companies using multiple funding sources and running structured processes were 40% more likely to report successful rounds above five million dollars compared to founders running unstructured single track processes. Elena was structured almost to a fault and the investors she was talking to noticed it because it told them something important about how she would run the company after the check cleared.

She built the relationships before she needed them

The fourth thing is the one most founders can’t replicate quickly enough because it’s not something you do during a raise. It’s something you do in the twelve months before one.

2 of the 3 investors who ended up in Elena’s round had met her nine months earlier when she wasn’t raising. She’d shared a market insight that was genuinely useful. She’d followed up when something she predicted came true. By the time she officially opened the round those two conversations were formalities. The real decision had already been made.

What actually separated her

Elena didn’t raise because her company was exceptional in a market full of mediocre ones. There were better companies than hers that didn’t close. She raised because she understood something most founders don’t want to accept which is that the fundraise is a process you run and every process has inputs you can control and outputs that follow from them.

She focused on everything within her reach and let the market do the rest.

Elena is a composite character built from patterns observed across dozens of real founder fundraising journeys. She isn’t one person but she represents many.

🌱 New Venture Funds on the Street

Week of July 4-10, 2026

Paradigm Fund III has closed at $1.2B - the crypto pioneer’s pivot into a “technical frontier” thesis spanning AI, robotics and blockchain, with Zipline and True Anomaly already on the books. Founded by Matt Huang and Fred Ehrsam, it came in below a reported $1.5B target, which in a year when crypto prices sit near highs says plenty about where the sector’s fundraising stands right now.

B Capital has closed Ascent Fund III at a $500M hard cap, nearly double its 2022 predecessor, writing Seed to Series B checks across AI, healthcare, enterprise and energy in North America and Asia.

Chemistry has filed to raise Fund II at $500M, already oversubscribed and doubling the $350M debut of the ex-Index, Bessemer and a16z trio behind Granola and Decagon.

Fundamentum has launched Fund III at $260M, becoming India’s only pure-play Series B firm to reach a third vintage as Nandan Nilekani steps back to anchor.

Expeditions has closed Fund II at $230M, backing early-stage defence, AI, cyber, quantum and space across Europe, with BAE Systems, the EIF and the NATO Innovation Fund behind it.

Climentum Capital has held a first close of Fund II at $70M (targeting $115M), leading Seed and Series A climate hard tech rounds across the Nordics and DACH.

Pegasus Tech Ventures has launched a $50M FoodTech fund with Japan’s Ohayo Dairy as sole LP, targeting food, biotech and supply chain startups from Silicon Valley.

Omni Ventures has closed Fund I at $33M, oversubscribed, with two ex-Apple engineers writing pre-seed checks into manufacturing tech.

Catalyst Fund has raised $30M at the second close of Climate Resilience Fund I, backing early-stage climate adaptation startups across Africa.

Vermilion Cliffs Ventures has closed Fund II at $25M, up from a $13M debut, with solo GP Ashley Smith backing technical founders in AI infra, security and dev tools.

Genesys University Seed Fund managed by Genesys Capital has held a first close of over $22M on the Genesys University Seed Fund, backing Ontario life sciences spinouts from U of T and McMaster.

💸 Who Got Funded This Week

🏔️ Growth & Mega Rounds

Joulent $1.75B Strategic · Large-scale energy and grid infrastructure for compute-heavy demand

SambaNova $1B Series F · AI inference chips and on-prem compute infrastructure

LeapXpert $180M Growth · Compliance and monitoring layer for enterprise messaging channels

Robotera $148M Strategic · Humanoid robots for logistics and industrial automation

Oxylabs $130M Growth · Web-data and proxy infrastructure for AI agents

Premier Lacrosse League $100M Strategic · Professional field lacrosse league and media operation

🌴 Series C+

Together AI $800M Series C · Cloud platform for training and running open-source AI models at scale

Norm AI $120M Series C · AI agents that automate legal and regulatory compliance

Taktile $110M Series C · Agentic decisioning platform for banks and insurers

Pearl Health $110M Series C · AI platform for providers managing Medicare populations in value-based care

Higharc $95M Series C · AI platform for homebuilding, from design to construction documents

Flare Therapeutics $85M Series C · Transcription-factor drug discovery for cancer and other diseases

🌲 Series B

Kraken Technology Group $175M Series B · Uncrewed high-speed maritime-defence vessels

Even Realities $150M Series B · Camera-free AR smart glasses

Quaise Energy $134M Series B · Superhot millimeter-wave drilling for deep geothermal

Twelve Labs $100M Series B · Multimodal AI models that search and analyze video

Venus Aerospace $91M Series B · Rotating detonation rocket engine for hypersonics

Ollama $65M Series B · Open-source framework for running LLMs locally

Straiker $64M Series B · Security testing and monitoring for AI applications

Aligned $60M Series B · Digital sales room and buyer collaboration workspace for B2B teams

Deruizhiyao $52M Series B · AI-driven drug discovery platform

Auger $50M Series B · AI platform for supply chain operations

🌳 Series A

Proxima Fusion $468M Series A · Stellarator nuclear-fusion reactor

Oratomic $300M Series A · Neutral-atom fault-tolerant quantum computing

8090 Solutions $135M Series A · AI-native software factory where human and agent teams build enterprise software

Prime Intellect $130M Series A · Decentralized compute and RL frameworks, an "AI lab in a box"

Beeline Medicines $126.3M Series A · Autoimmune therapeutics spun out of a five-program license

Venice $65M Series A · Private, surveillance-free access to AI models

Qolab $54.2M Series A · Superconducting quantum computing systems

Bespoke Labs $40M Series A · AI evaluation, developer tools, and AI infrastructure

🌿 Seed

Monogram $40M Seed · Voice-driven generative-UI app that builds dynamic interfaces, not text

Find more deals and detailed backers below:

💰 Who Cashed Out This Week?

🚀 Pipeline Watch

#1 · Blue Origin · $10B raise · $130B valuation · July 8

First outside capital in 25 years of Bezos self-funding. Coatue leads with $4B, Bezos himself puts in $2B. SpaceX’s IPO changed the math for everyone in space.

🪙 Jeff Bezos (Founder), Dave Limp (CEO, Blue Origin), Philippe Laffont (Founder & CIO, Coatue Management)

#2 · SpaceX (SPCX) · Joins Nasdaq-100 · July 7

Fastest ever Nasdaq-100 inclusion - just 15 trading days post-IPO. $4.3B in forced passive buying from $800B in index-tracking funds. Every QQQ holder now owns SpaceX whether they intended to or not.

🪙 Elon Musk (Founder & CEO), Gwynne Shotwell (President & COO), Antonio Gracias (Valor Equity), Luke Nosek (Founders Fund), Peter Thiel (Founders Fund)

#3 · Columbus Circle Capital III (CCCTU) · $200M SPAC IPO · Nasdaq · July 9

Cohen & Company’s third blank-check vehicle hunting AI infrastructure, crypto, sports or energy-transition targets across North America, EMEA and LatAm. Nobody gets rich yet - this is blank-check money.

🪙 Gary Quin (CEO & Chairman), Joseph W. Pooler Jr. (CFO), Daniel Cohen (Cohen & Company)

#4 · Mercator Acquisition Corp · $150M SPAC IPO · July 9

Hondius Capital’s blank-check pool targeting a fintech acquisition. Same caveat - contingent on finding a target.

🪙 Shawn Matthews (Chairman & CEO, Hondius Capital), Steven Bischoff (CFO)

📈 IPO Debuts

#1 · SK Hynix (SKHY) · $26.5B · Nasdaq · July 10

Largest US listing ever by a foreign company, beating Alibaba’s 2014 record. 7x oversubscribed. Priced at $149, opened at $170, closed +13%. Controls 56% of global HBM market that every AI chip depends on.

🪙 Chey Tae-won (Chairman, SK Group), Kwak Noh-jung (CEO, SK Hynix)

#2 · Momenta Global · $752M · HKEX · July 8

Chinese autonomous driving startup backed by GM, Tencent, Mercedes-Benz, Toyota, and BYD. Retail tranche 413x oversubscribed. Closed 2% below IPO price - a reality check for loss-making AV companies.

🪙 Cao Xudong (Founder & CEO, Momenta)

🤝🏻 M&A

#1 · Thales acquires Exail Technologies · ~$4.4B (EUR 3.9B) · July 6

France’s Thales grabbed submarine-drone maker Exail for $4.4B, betting the next drone war happens underwater. Family-controlled business, not a VC exit - but the largest defence deal of the week.

🪙 Raphaël Gorgé (Chairman & CEO, Exail / Groupe Gorgé), Exail public shareholders

#2 · Lockheed Martin acquires Ultra Maritime · $3.45B · July 6

Sonar systems, sonobuoys, and autonomous maritime sensing. Carved out by Advent in 2022, sold 4 years later at a significant step-up after $170M in product development. PE exit, not a founder exit.

🪙 Shonnel Malani (Managing Partner, Advent International), Carlo Zaffanella (President & CEO, Ultra Maritime)

#3 · Novartis acquires Myricx Bio · Up to $1.5B ($1.1B upfront) · July 6

Imperial College London spinout, founded 2019, raised $114M, sold for ~13x in 7 years. Sofinnova Partners’ seventh exit in three years.

🪙 Mohit Rawat (CEO), Prof. Ed Tate, Roberto Solari, Andrew Bell (Co-founders), Robin Carr (CTO), Michael Bauer (Novo Holdings)

#4 · Nurix AI acquires Verloop.io · Undisclosed · July 9

Bengaluru’s Nurix AI bolted chat automation onto its voice-AI stack by acquiring Verloop.io. Founder staying on rather than cashing out fully.

🪙 Gaurav Singh (Founder, Verloop.io - joining Nurix leadership)

📊 Your Reading List For The Week

Fresh VC-focused blogs & research:

Venture Capital Archive (List): New Venture Funds - June 2026 - Read more

Venture Capital Archive (List): Top 25 VC and Startup Influencers You Should Be Following - Read more

Venture Capital Archive (Blog): Bad VC - Read more

Venture Capital Archive (Blog): 5 Things First-Time Founders Must Remember When Working With VCs - Read more

PitchBook (Report): Q2 2026 PitchBook-NVCA Venture Monitor - Read more

Gritt (Blog): Venture Capital Deal Sourcing - Read more

Sifted (Article): Yann LeCun is Starting a VC Firm - Read more

Fortune (Article): The 38-Point Framework Two VCs Use to Spot the Next Unicorn Founder - Read more

🎙️ Podcast picks

Insights from Industry Leaders

Innovators & Investors: Transforming the Real Sector with Decision Intelligence - Listen here

This Week in Startups: Episode - Listen here (can you confirm the episode title?)

The Full Ratchet: Best LP Questions From David Ulevitch, Eric Ries and Larry Cheng - Listen here

VC Unfiltered: How to Raise Venture Capital - AI Startup Pitches and Investor Insights - Listen here

The a16z Show: Adam Neumann - This is How You Build Iconic Companies - Listen here

Invest Like the Best: Jeremy Giffon - The Billion Dollar PDF - Listen here

The European VC: Alex Manson - SC Ventures, Corporate Venturing is More Than CVC - Listen here

Kstreet VC: How VCs Evaluate Pre-Revenue Startups - Paige Soya and Nick - Listen here